An Explainer of our Global Oil System and its Consequences

Curriculum Specifics

- Courses: Economics, History, Sociology

- Educational Level: High School Advanced, Introductory College Level

- Reading Level: 12th Grade+ (This one is tough. A Glossary is provided)

- Reading Time: 15 minutes

The Background

Are you driving? You may have noticed that filling that tank is a bit more expensive. Or maybe you are listening to your parents grumble a bit more at the gas station. Maybe you’re wondering what’s going on.

Yeah! What the heck!

We are currently involved in major military operations that is impacting the world’s most significant oil producing nations, and one of the world’s most active oil trade routes. To understand what’s going on with your wallet, you have to understand what’s going on in the world and the system that guides it.

For over a hundred and twenty years, oil has been the backbone of the global economy. For decades, oil fueled just about everything from our gas tanks to our communities, from our factories to our jets. Then there’s the rise of petrochemicals and plastics that literally hold our global economy together. Our industries were fueled by oil. Our armies were fueled by oil. So long as the oil was flowing, the international marketplace and the regional economies it supported, continued to produce.

Most importantly, American economic centrality was sustained.

Wow!

That’s a pretty big lift for a single commodity. As the core nations industrialized, and developing nations demanded their share of the Industrial Pie, the efficient transmission of oil from places where it was pulled from the ground, or under the sea, to refineries, to widely dispersed marketplaces became a matter of foremost concern.

We learned this the hard way in the 1970s. In 1973, Arabian oil producers put an embargo on the U.S. in response to its support for Israel, strangling an already struggling economy. In 1979, the Iranian Revolution choked off Middle Eastern oil exports. I’m old enough to remember the long lines at the gas stations. In Rhode Island, where I grew up, gas was rationed according to the numbers on one’s license plate, with even and odd numbers allowed to purchase gas on alternating days. No gas could be purchased on Sundays. It was ugly.

Yeah. My grandparents told me something about that!

Ouch!

Anyway…

This oil shortage exacerbated an already existing economic crisis in the United States, not so affectionately referred to as “Stagflation,” high inflation at the same time as low economic growth and unemployment.

This stagflation mess was accelerated by the fall of the first Bretton Woods System. Bretton Woods was a global economic arrangement by which all participating nations pegged the value of their currency to the dollar, and the dollar was set to the gold standard. This worked great for a while. So long as the United States was the major exporter after World War II blew up the competing exporters, it seemed like it would last forever. Eventually, however, those exporters got up and running again and started exporting again. They were exporting some pretty good stuff, and Americans who were pretty well off started buying that stuff. Which meant a lot of dollars accumulated in a lot of countries…all of it redeemable in gold.

This became a serious problem by the late 1960s, convincing then President Richard Nixon that the gold standard was unsustainable. A global economy, with the United States as its hub, required more financial flexibility than the gold standard could vouch. It only took the United States forty years to realize that John Maynard Keynes was correct in his assessment that, “In truth, the gold standard is already a barbarous relic.” Coming off the gold standard, however, had its consequences. The dollar became a fiat currency, and all those currencies pegged to the dollar were free floating, adding a great deal of uncertainty to the global financial marketplace.

Oil was the solution. In the mid 1970s, President Nixon negotiated what became known as the Petrodollar Accord with Saudi Arabia.

Get this! This is going to blow your mind!

First, Saudi Arabia, as the leading nation in OPEC would price all of its oil exports in U.S. dollars. Think about this. With some few exceptions,1 if China wants to buy oil from the global market, it must do so in dollars rather than its own currency, the Yuan. Secondly, Saudi Arabia agreed to reinvest much of the dollars it was going to pile up as a result of this arrangement into U.S. Treasury Bonds. So, a nation like China must open its markets to U.S. dollars if it wants oil. It then uses those petrodollars to purchase oil from OPEC and other oil producers in a global exchange. Many of those dollars then come back to the United States in exchange for funding the U.S. debt. Thirdly, and this is the one you are not going to believe, the United States guaranteed, the perpetuation of the Saud Dynasty as the perpetual dictators of Arabia…Saudi Arabia.2

Holy Cow! So, to buy oil, other countries need dollars because Saudi Arabia says so!

Are realities starting to open up?

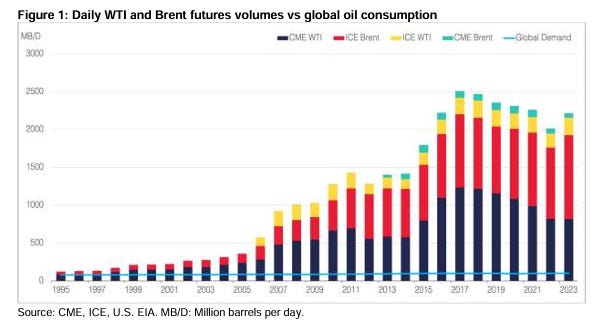

The rise of petrodollars also corresponds to the institutionalization of the global oil exchange. Oil producers, retailers, and investors needed systems in place to stabilize distribution of this all important product. By the 1980s we see the emergence of the global oil market that we have today with companies investing in oil contracts through exchanges controlled by agencies like WTI and ICE Brent.

How this Works

The evolution of this modern oil market worked. Since the 1980s we really haven’t seen the kind of oil shocks that we witnessed in the seventies. We’ve seen prices rise and fall, but the oil continued to flow to the places where it was needed. Consequently, it’s a good idea to understand how this process works. Let’s take a look at the oil market from sinking the wells to filling your tank.

First, oil has to be extracted from the earth. Once upon a time, this was relatively cheap. When Edwin Drake dropped the first productive oil well in Titusville, Pennsylvania in the middle of the nineteenth century, oil was kind of a nuisance. It would seep up out of the ground and make everything all gooky. Those days are gone. Now, the physical process of oil extraction can be quite expensive. In the United States, the average cost of extraction ranges from $30 to $70 a barrel. If oil trades at around $70 a barrel, oil producers see little incentive to invest in new wells or to increase production.3

When the price per barrel increases as a result of, oh I don’t know, a major war in the Middle East, oil producers have an incentive to drill.

Um…!

Just sayin’.

Once the oil is pulled from the ground it is stored temporarily until sold. This is where it gets a bit confusing. There are two kinds of oil purchases. Of course, there is the physical oil purchase. This is the intuitive one that is easy to understand. A refiner or middleman purchases X-number barrels of oil. After this firm purchases the oil it does with it whatever will bring the best profit. At that point the oil goes into a pipeline or oil tanker for distribution.

The second kind of purchase is the futures or derivatives contract.

I don’t like the sounds of that!

It’s a bit complicated. just bear with me.

Believe it or not, this is where the action is. Over 95% of all oil purchases made are made through the global exchanges like Brent and WTI in the form of these contracts. It’s kind of a New York Stock Exchange, but for oil. A futures contract is simply a promise to deliver or accept delivery of a certain amount of oil at a given price. If I’m a investor and I see oil selling at $75 a barrel, but I believe the price of oil will go up to $85 a barrel in a year, I might enter a futures contract at today’s price, otherwise known as a short. Or, if I’m an oil purchaser, and I think the price of oil might fall, I might enter a contract to purchase at the future price, (a long). Obviously, if I’m wrong on either end, I could lose a lot of money. It’s a bet on future prices.

No oil is moving anywhere as a result of these transactions. It’s all “paper oil” at this point. I may hold a short position on oil for $75 and sell it the next day for $76 to another investor, who then turns around and sells it for $77. This can happen hundreds of times before the last firm holding the paper must either deliver or take possession of the actual oil. It’s like a game of hot potato. This is why the volume of oil sales far exceeds the actual amount of oil in the market.

A bit confusing, but okay.

This is also why the price of oil is determined by the exchanges and not the actual physical supply and demand of the oil. Futures investors need a stable financial system on which to place their bets. Consequently, they use Brent, WTI, or Dubai as benchmarks for the market as a whole. When the future price seems greater than the spot price, or the current price, there is an incentive to hold on to the oil, to store it, thus driving up current prices. This is called a Cantango. On the other hand, we may see what’s called Backwardation, when the future price seems to be lower than the spot price. This encourages getting rid of existing stores, selling of supply, and drives prices down. Such predictive variables have to do with the state of global or regional conflict, like a war with Iran that threatens to close the Strait of Hormuz, new oil finds, new technologies, or any phenomenon that might alter the direction of oil prices.

At some point, however, every futures contract comes due. Whoever is holding the paper at the end must fulfill their agreement to deliver or accept delivery of the oil. Oil on a tanker headed to a refinery in Garyville, Louisiana may find its destination changed to São Paulo, Brazil. That it was drilled in the United States does not mean it will be refined or sold in the United States. In São Paulo, that oil will be refined into gasoline. Some of that gasoline may be placed on a train and shipped to Ecuador. It may even be sold back to an American firm and shipped to my local Racetrack where I’ll pump it into my tank.

This seems awfully complicated, but this system has guaranteed the continued flow of oil based on demand. Yes, we have experienced price shocks, such as in 2007, and 2011 that made us grumble. However, the oil still flowed. There were no rations and long lines4 impacting the whole economy.

The Consequences

Every benefit carries a cost. For instance, when gas prices are high, some politicians shout, “Drill! Drill! Drill!” from the mountaintops. This makes intuitive sense, but it won’t work. It won’t work because oil firms won’t drill if the prices drop too much. Furthermore, if the American firms increase production, other firms may decrease production and purchase from the exchange. This benefits them because they are trading in oil that they did not have to spend money to extract. But it also reduces or stabilizes the supply so that there is no net benefit to prices since there is no net change in production at the global level on which prices are determined.

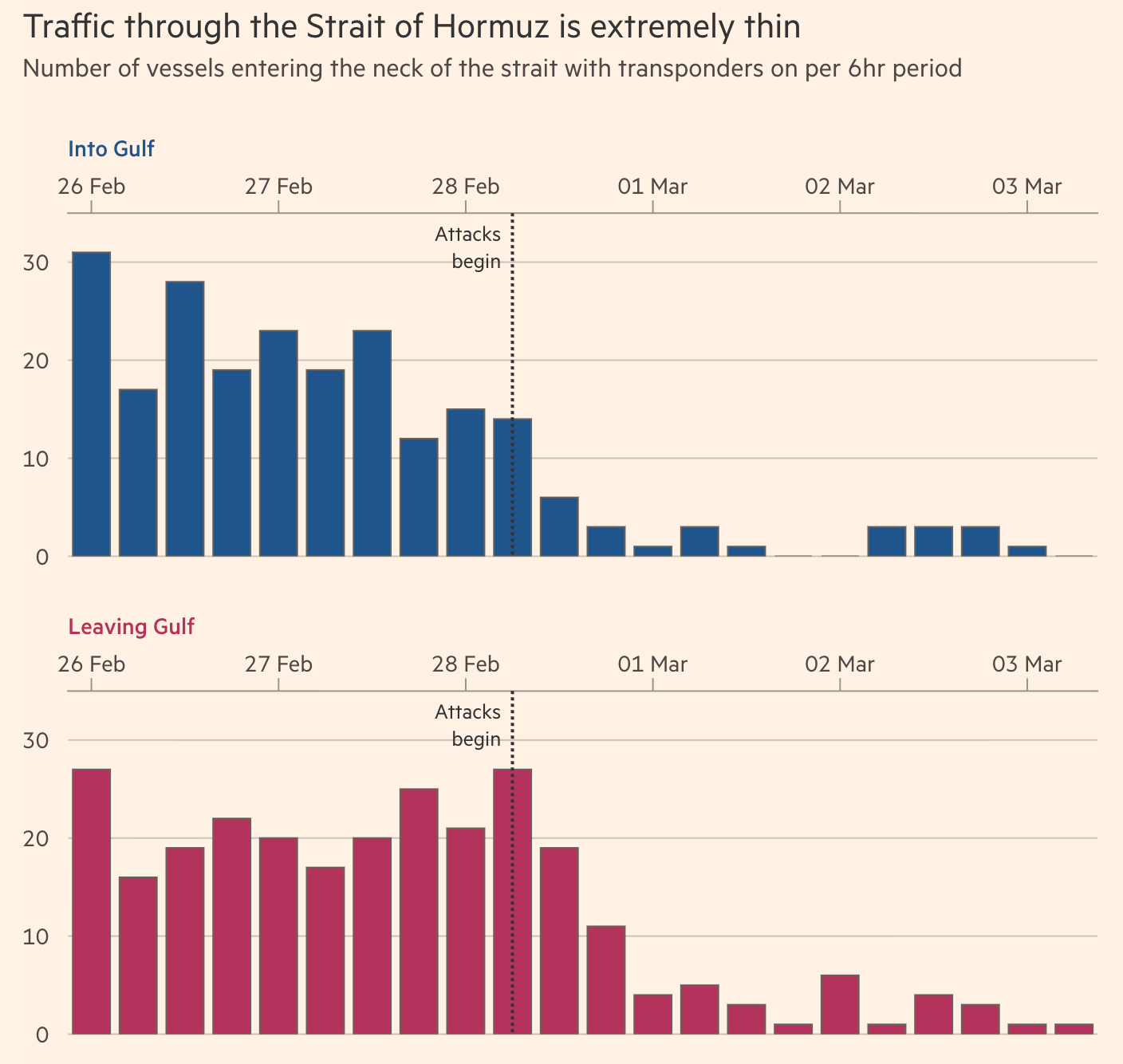

The most immediate consequence of concern to you is, of course, the impact of the Iran War. Oil passing through the Strait of Hormuz constitutes about twenty percent of global consumption and almost thirty percent of all maritime oil trade. Most of that trade physically goes to Asia. If Asia, however, can’t get its oil from the Middle East, it will bid up in other areas to attract what they need. This will drive up prices throughout the world. And increased oil prices mean increased fuel prices. Most of the goods we receive are transported. We can expect to see an increase not only in our gas tank, but in overall inflation.

Nice! How much?

Well, that’s the good news. It will pinch, but we are not talking about seventies gas lines or stagflation. Paul Krugman’s “back of the envelop calculations,”5 puts the direct cost at about a .3% increase in consumer prices for an increase of $15 per barrel of oil. A one percent increase for a $50 increase per barrel. That’s doable. We’ve recently been through worse inflation.

That being said, promises to reduce inflation were made…this war does not reduce inflation.

There is one more cost, however, that often never makes it to the publicly discussed ledger. Shipping through the Strait of Hormuz will have to be protected. In other words, military vessels will be needed to guard civilian vessels if oil transport is to be restored and continued. Who do you suppose will foot the bill for that?

Don’ say, you and me.

Well, what are the chances the government will raise taxes on the billionaires in order to fund this war?

…

Yeah, that’s what I think, too. So, we are looking at more debt, which means higher interest on the national debt. Less money for everything else. It also means higher interest on our own debt. One way or the other, working people will pay the short-term costs spread out over the long term.

Just in time for you to get that credit card!

To describe other long-term consequences of our modern oil market, however, we need to understand why the impact of the Iran War is much smaller than the Embargo in ‘73, or the Iranian Revolution in ‘79. The fact is that we are not as dependent on international oil as we were in the seventies. First, almost none of our domestic electricity requires oil. Most of our electric generation is coming from natural gas or renewables. For the United States and most other advanced nations, oil is used mostly for transportation, for filling tanks.

Well, that’s something!

Now, here’s where it gets dicey.

Of course it does!

The fact mentioned above should be a golden argument for even further investment in alternative energy and especially electric vehicles. I have a truck, and I’m not happy about the prospects for gas. However, I also have an EV. So, worst case scenario for me is using the EV more. Theoretically, a nation that “completely” transitions6 to alternative energy will not even give a second thought to conflicts in the Middle East.

However, the United States is a special case. Our currency, the global reserve currency, and our centrality to the global economy depends on oil. Remember, for the most part, the oil market is mediated with dollars. As alternative energy replaces oil energy, demand for oil will decrease. If the demand for oil decreases, the demand for dollars decreases. This doesn’t just impact oil companies. It impacts all American financial interests.

Why is the United States, the world’s wealthiest and most powerful country, the only culture in the world to sneer at the scientific fact of global warming? Because American power rests on global warming being a hoax, protecting those petrodollars, and sustaining American economic centrality.

That doesn’t seem sensible.

It’s not. This system cannot last. One way or the other, it will fall and be replaced with something else. Most likely it will be replaced by a system in which the United States is no longer the fulcrum of global balance. There are a lot of powerful interests who depend on that particular seesaw.

This essay actually started as a short social media post on rising gas prices. The reality is that this conflict goes beyond our apprehension at the gas tank. To really understand what is going on, we must understand the global system in which it is happening. Frankly, this structure is failing. It is, to steal from Keynes, a barbaric relic. Powerful interests may be willing to kill millions of people to sustain their wealth and power, but the system will fail. That begs the question, what will replace it? Will it be a more democratic and human system, or will we fall into an even more treacherous and barbarous hegemony than we have?

The answer to these questions will hinge on whether or not the global ecosystem collapses first.

Glossary

Bretton Woods System

A global financial system created after World War II where countries tied their currencies to the U.S. dollar, and the dollar was tied to gold. It collapsed in the early 1970s.

Cantango (Contango)

When the future price of oil is higher than the current price, encouraging companies to store oil and sell it later.

Backwardation

When the future price of oil is lower than the current price, encouraging companies to sell oil now instead of storing it.

Commodity

A basic good that can be bought and sold in large amounts, like oil, wheat, or copper.

Derivatives

Financial contracts whose value comes from something else, such as oil prices. Futures contracts are a common type.

Even/Odd Gas Rationing

A system used during the 1970s oil crisis where people could only buy gas on certain days based on the last number on their license plate.

Fiat Currency

Money that has value because the government says it does, not because it is backed by gold or silver.

Futures Contract

An agreement to buy or sell a set amount of oil at a specific price on a future date. Most oil trading happens through these contracts, not through physical barrels.

Global Oil Exchange

The worldwide system where oil is traded, both physically and through financial markets.

Gold Standard

A monetary system where a country’s money is backed by gold. The U.S. ended this system in 1971.

Hegemony

A situation where one country has major influence or control over others.

Inflation

A general rise in prices across the economy, meaning money buys less than before.

OPEC (Organization of the Petroleum Exporting Countries)

A group of major oil‑producing nations that coordinate production and influence global oil prices.

Petrochemicals

Chemical products made from oil and natural gas, used to make plastics, fertilizers, and many everyday items.

Petrodollar System

An arrangement where oil is priced and sold in U.S. dollars. This keeps global demand for dollars high and strengthens U.S. economic power.

Reserve Currency

A currency held by many countries for international trade and financial stability. The U.S. dollar is the world’s main reserve currency.

Saudi Dynasty / Saud Family

The ruling royal family of Saudi Arabia. The U.S. has historically supported their rule in exchange for stability in oil markets.

Spot Price

The current price of oil if you buy it right now.

Stagflation

A rare economic situation where inflation is high and economic growth is low at the same time. This happened in the U.S. during the 1970s.

Strait of Hormuz

A narrow waterway between Iran and Oman through which about 20% of the world’s oil supply travels. Conflicts here can disrupt global oil prices.

WTI (West Texas Intermediate)

A major U.S. oil benchmark used to set prices in global markets.

Footnotes

- There are oil producing nations that allow China to purchase oil using Yuan. Namely, Russia, Venezuela, and Iran…Oh! Wait! ↩︎

- Consequently, Saudi Arabia can be as shitty as it wants to be and never have to worry about reprisals from the United States. The Saudi royal family can literally cut up a resident American journalist and, “Meh. Bad things happen.” ↩︎

- This is why political promises to “Drill, Baby, drill!” are hollow. Increased drilling leads to increased production, leads to lower prices. Lower prices, however, disincentivize investment in further drilling. Market forces outside of any president’s control will balance the market. The president can lease all the oil fields he has. If the incentive to drill isn’t there, this will make no difference. ↩︎

- With the exception of hurricanes and such ↩︎

- Far more accurate than my front of the envelope guesses! ↩︎

- Relax! It’s hypothetical to make a point. We’ll need some kind of oil production no matter how completely we transition to renewable energy. We’ll need backup generation for emergency situations. Also, not all oil goes to energy. A great deal goes to petrochemicals and lubricants. ↩︎

1 Comment